Introduction: UK borrowing surges over forecasts in May

Good morning, and welcome to our rolling coverage of business, the financial markets and the world economy.

The health of the British economy is centre stage today, as Andy Burnham wins the Makerfield by-election and declared that the Labour party has a “final chance to change”.

But the latest public finances, just released, show the challenges facing whoever is in Downing Street.

Britain borrowed £23.3bn in May to cover the difference between government income and spending – a surge of £5.4bn more than a year ago.

That’s the highest borrowing for any May since 2020, when the Covid-19 lockdown was in force.

Worryingly, it’s also £5.6bn more than the £17.7bn forecast by the Office for Budget Responsibility (OBR), the UK’s fiscal watchdog.

This means government borrowing for this financial year (since April) is running £7.7bn over the OBR’s forecasts – at £46.3bn.

That raises the risk that borrowing could be higher than forecast by the next budget, risking breaking Rachel Reeves’s fiscal rules – unless, of course, there is a leadership battle, and a new chancellor by the autumn…

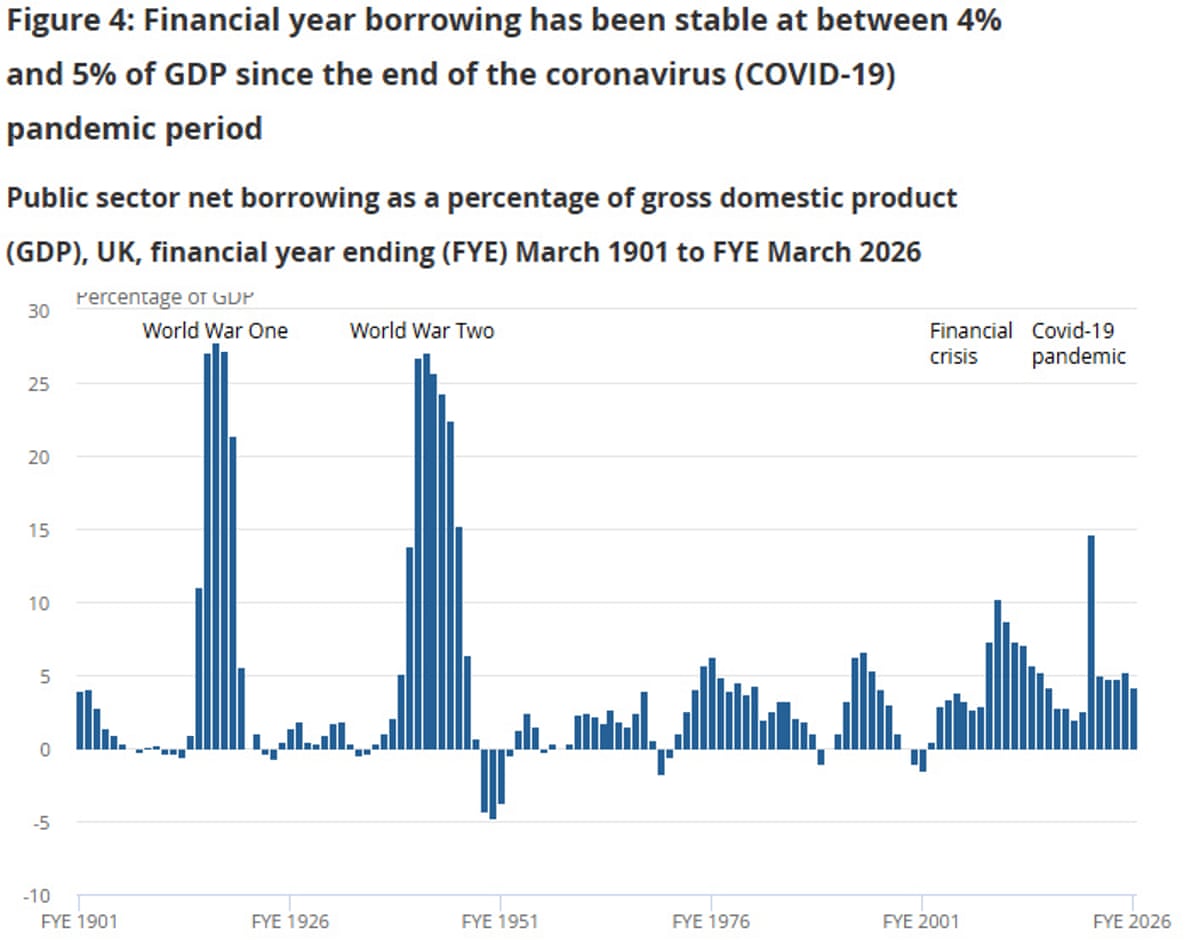

The bigger picture is that this pushes the UK’s national debt up to 95.1% of GDP, levels last seen in the early 1960s.

“Borrowing in the first two months of the financial year was nearly £9 billion higher than the same period of 2025.

Spending on debt interest, public services, investment and benefits all increased in May 2026, compared with last May, more than outweighing higher tax receipts.”

— ONS senior statistician Tom Davies

The agenda

7am BST: UK retail sales report for May

7am BST: UK public finances report for May

11.30am BST: Bank of Russia interest rate decision

Why Andy Burnham’s by-election victory matters for the public finances

Martin Beck, chief economist at WPI Strategy, has warned that the underlying picture of the UK public finances “remains uncomfortable”, even if the US-Iran deal helps to ease inflation.

“The deficit is still large, debt interest is still absorbing a painful share of revenue, and the tax burden is already heading for post-war highs. There is no easy escape route through either borrowing or taxation.

That is why Andy Burnham’s by-election victory matters for the public finances. It does not change the arithmetic overnight, but it changes the politics around the arithmetic. A serious Labour leadership challenge would raise a simple question for markets: is the governing party about to shift towards higher spending, looser fiscal rules and a more relaxed attitude to borrowing?

Burnham’s past argument that governments should not be “in hock” to bond markets may play well politically, but it is not a fiscal strategy. Any Prime Minister inheriting an annual deficit of well over £100bn would quickly discover that the gilt market is not an optional audience.

Beck concludes that the gilt market is now the hard constraint on British politics:

“A Burnham premiership might change the language of economic policy, but it would not abolish the arithmetic. The next Labour leader, whoever it is, will still face the same brutal equation: weak growth, high borrowing, expensive debt and very little room for manoeuvre.”

UK borrowing: what the experts say

Emeritus professor Joe Nellis, economic adviser at MHA, warns that the UK public finances are “not in comfortable territory”, after borrowing jumped by £5.4bn year-on-year last month:

“Public sector net borrowing came in at £23.3bn in May, showing the continuing pressure on the UK’s public finances and the difficult choices that lie ahead for the government and the Treasury for the rest of this financial year.

Borrowing in May was only slightly below the exceptionally high level recorded for April, remaining very high by historical standards. The latest data once more highlight the difficulty of balancing public-sector spending requirements with the government’s pledge to keep public finances on a sustainable path.

A number of factors continue to weigh heavily on the fiscal position. Debt interest payments remain elevated, public services are under significant strain, and weaker economic growth risks limiting the pace of tax revenue growth into the Treasury coffers. At the same time, seemingly unending demands for more and more spending, particularly on health, defence and infrastructure, show little sign of easing up.

The implications reach far beyond just the monthly borrowing numbers themselves. The figures will shape expectations about the Chancellor’s room for manoeuvre ahead of the Autumn Budget and will influence decisions on taxation, public spending and borrowing for the remainder of the financial year. The UK is far removed from the extraordinary borrowing levels seen during the pandemic, but the public finances are not in comfortable territory.”

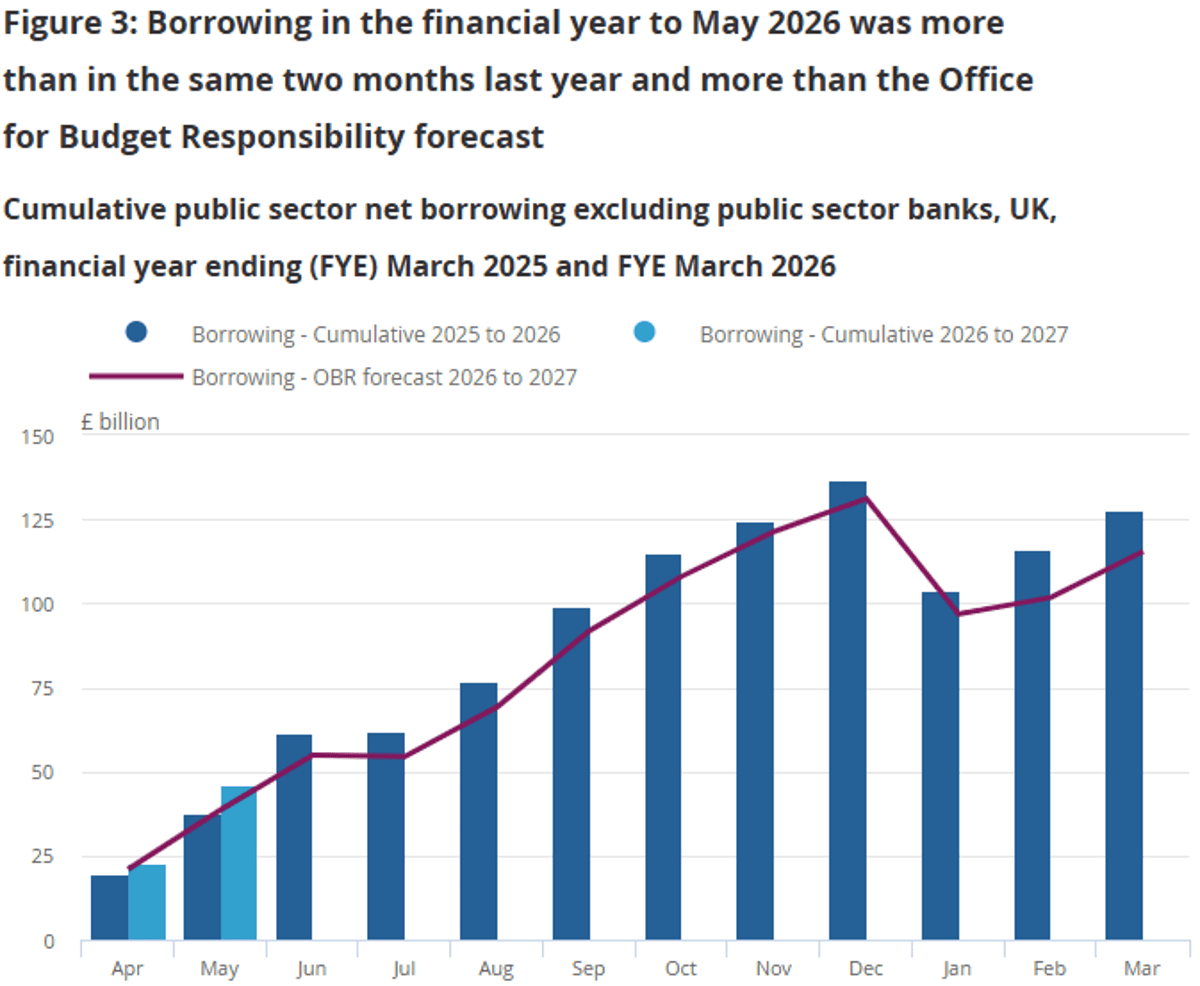

This chart shows how UK government borrowing has been higher so far this financial year (light blue) than in the 2025-26 financial year (dark blue).

How government spending rose in May

Today’s public finances report also shows how inflation drove up the cost of servicing the national debt in May.

The Office for National Statistics reports that the debt interest bill increased by £4.1bn to £11.7bn, due to movements in the Retail Prices Index (RPI) of inflation.

Government spending on services, and benefits such as pensions, both rose too:

Central government departmental spending on goods and services increased by £2.2bn to £39.6bn, as inflation increased the cost of providing public services.

Net social benefits paid by central government increased by £1.2bn to £28.4bn; this was largely caused by inflation-linked increases in many benefits, and earnings-linked increases to State Pension payments.