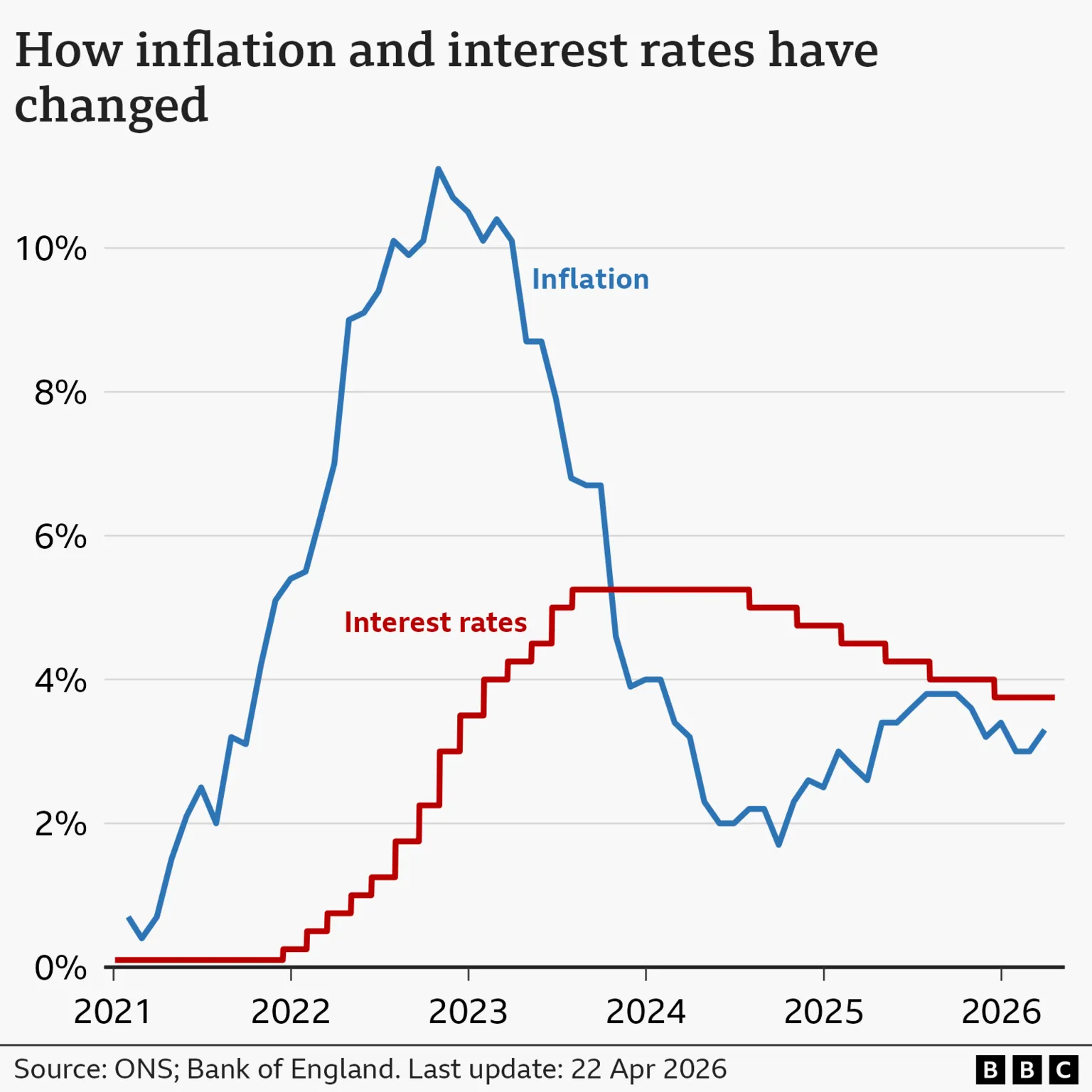

It is becoming increasingly evident how a conflict thousands of miles away is affecting finances in the UK, with the latest data indicating that inflation has increased to 3.3% over the year to March.

Petrol and diesel prices have reached their highest levels in more than three years; however, the overall impact of the war on inflation has been relatively limited.

With warnings of potential rises in food prices and travel costs on the horizon, questions remain about how high inflation might climb and what implications this could have for borrowers and savers nationwide.

Here are three key points to consider.

It's not only up from here

The increasing expense of fuel at the pumps may create the impression that inflation will continue to rise, at least in the short term. However, this is not necessarily the case.

For example, the inflation figures for April may show a different trend. The domestic energy price cap was reduced this month, reflecting market conditions from several months prior due to the lag in adjustments. This means the average household energy bill for typical gas and electricity usage will decrease by approximately £10 per month starting this month, exerting downward pressure on inflation.

It is important to note, however, that energy bills are expected to rise again with the next price cap adjustment in July, largely due to the ongoing war.

Fuel prices themselves have started to decline slightly in recent days as oil prices have stabilized, though petrol remains about 25p per litre higher than pre-war levels, and diesel is over 40p more expensive.

Additionally, the increase in airfares recorded in March's inflation figures was influenced by the timing of Easter. This year, the return leg of long-haul flights monitored had a return date on the Tuesday after Easter Sunday, coinciding with peak season. Since airfare data was collected in February, before the war's impact, these figures do not reflect wartime effects.

Typically, when Easter falls early, inflation figures show a decrease in airfares the following month.

These factors have led analysts to predict that inflation could potentially fall below 3% in April.

Analysts estimate that inflation may peak near 4% this year, significantly lower than the 11% peak observed in 2022 at the onset of the war in Ukraine.

But food prices could have a way to go

Similarly, the recent rise in food inflation appears to have a seasonal component, concentrated in Easter-related items such as confectionery and meat.

Nevertheless, caution is advised as other price pressures may emerge more gradually.

Food producers typically purchase inputs most affected by the war, such as energy and fertilisers, months in advance, meaning it can take a year or more for price changes to be reflected in supermarket shelves.

The food and drink industry, including supermarkets, is energy-intensive and thus vulnerable to higher energy costs.

The Food and Drink Federation has warned that its members could increase prices by 9 or 10% by the end of the year, although this outcome is not certain.

Consumers are currently more financially constrained than in 2022, cautious after years of rising prices, and wary of spending due to challenges in the job market.

Many shoppers have already shifted to more affordable options to manage their budgets. Consequently, retailers may find it difficult to pass on higher costs through price increases without risking loss of customers.

Furthermore, prices of key food commodities such as wheat have not surged as dramatically as before, since supply risks are lower; Ukraine remains a significant supplier of staples including wheat and sunflower seeds.

So where does that leave interest rates?

The Bank of England's mandate is to reduce inflation to its 2% target and maintain it there. Prior to the war, with inflation expected to decline, interest rate cuts appeared likely.

However, circumstances have changed considerably. Early in the war, some predicted multiple rate increases due to inflationary pressures.

The Bank has indicated it will adopt a cautious and pragmatic approach, recognising that higher interest rates cannot influence global energy prices.

An energy price shock can reduce consumer spending and economic growth; raising rates could exacerbate these effects.

Given recent stabilization in oil and gas prices, economists increasingly believe the Bank will assess the duration of inflationary impacts before deciding on rate changes. This suggests a rate change at the upcoming meeting is unlikely.

As expectations for rate hikes have diminished, fixed mortgage rates have begun to ease after rising sharply in the past month. Borrowing costs remain a significant factor affecting not only homeowners but also landlords and tenants.

However, if interest rates remain unchanged this year, savers will see no improvement in their returns.

Much uncertainty remains as the war continues, but one positive note is that for most households, incomes have recently increased faster than prices.

Although it may not feel evident, the financial squeeze for many has eased, though the future outlook remains uncertain.