Wage Growth and Tax Threshold Freeze

Wages have been increasing faster than prices for the past two and a half years, marking the longest period of real wage growth since the 2008 financial crisis.

However, despite rising salaries, you may face higher tax payments due to frozen tax thresholds, a policy extended by the UK government in its Autumn Budget to remain in effect until 2031.

Use our calculator below to understand how your earnings might be affected.

The calculator is applicable to employees in England, Wales, and Northern Ireland. Scotland has different tax bands, and self-employed individuals are subject to different tax rules.

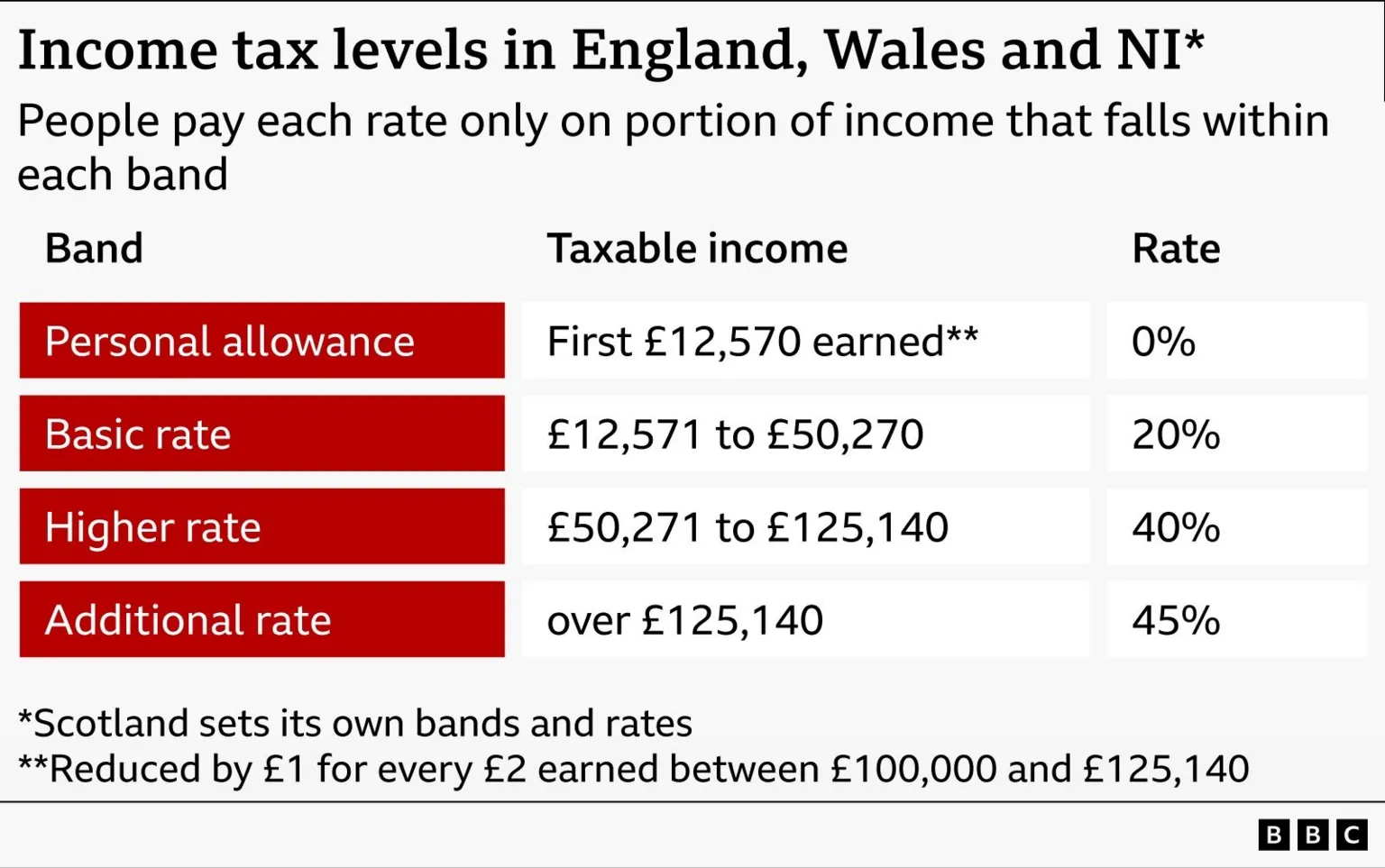

Understanding Tax Thresholds

Tax thresholds determine the income levels at which you begin paying higher rates of income tax and National Insurance as your salary increases.

You pay no income tax on the first £12,570 of your earnings, known as the personal allowance.

Income between £12,571 and £50,270 is taxed at 20%, referred to as the basic rate. Earnings between £50,271 and £125,140 are taxed at 40%, the higher rate. Any income above £125,140 is taxed at 45%.

If your income exceeds £100,000 after accounting for specific tax reliefs, your personal allowance is reduced by £1 for every £2 earned over that threshold.

Historical Context and Current Trends

Traditionally, governments have increased tax thresholds in line with inflation to help ensure that take-home pay keeps pace with the cost of living.

According to the latest data from the Office for National Statistics (ONS), weekly earnings across Britain grew at an annual rate of 0.8% between October and December after adjusting for inflation.

This indicates that average salaries have consistently outpaced price rises since July 2023.

Despite this, tax thresholds have been frozen throughout this period and are set to remain unchanged into the next decade.

Financial Impact of the Freeze

Our calculations reveal that the freeze in tax thresholds will add £465 to the combined income tax and National Insurance bill for an individual earning £39,000, which corresponds to the average UK salary in 2030-31.

Of this additional amount, £227 is attributable to the extension of the freeze announced by Chancellor Rachel Reeves in November.

For someone earning £50,000, the estimated increase in tax and National Insurance payments is £1,309, with £704 of that due to the freeze extension from 2028-29.

Economic Perspectives on the Freeze

Freezing tax thresholds is often described by economists as a "stealth tax" because it increases government revenue without raising tax rates.

Both Labour and Conservative governments have employed this strategy to generate additional funds, which support public services including the NHS, education, and welfare programs.

Most taxpayers will experience higher payments due to the freeze, but those whose salaries increase enough to cross into higher tax bands will see the most significant increases.

Government and Independent Analyses

The government has published an analysis of various tax and spending decisions since late 2024, including the effects of frozen tax thresholds. This analysis indicates that the lowest income households benefit, while the highest income groups lose out.

However, this government analysis only covers up to the 2028-29 period and does not include the extended freeze.

Research by the National Institute of Economic and Social Research (Niesr) shows that, in percentage terms, lower and middle-income households are most adversely affected by the freeze extension.

Timeline of Threshold Freezes

The freeze on tax thresholds was first introduced in 2022 by former Conservative Chancellor Rishi Sunak, initially set to last until 2026.

The Conservative government later extended the freeze for an additional two years, and Chancellor Reeves subsequently announced its continuation until 2031.

Projected Effects by 2030-31

The Office for Budget Responsibility (OBR) forecasts that by 2030-31, an additional 5.2 million people will be paying the basic rate of income tax due to the threshold freezes initiated in 2022-23.

Furthermore, 4.8 million more individuals are expected to pay the higher rate, and 600,000 more will pay the additional rate.

The OBR estimates that the frozen income tax thresholds will generate £56 billion in revenue in 2030-31, with £12 billion attributable to Reeves's extension.

Additional reporting by Lucy Dady and Jess Carr

How the Calculator Works

This calculator estimates the additional income tax and National Insurance contributions (NICs) you will pay in 2030-31 due to frozen tax thresholds.

It uses official forecasts from the OBR's November 2025 Budget to estimate the extra amount payable compared to a scenario where thresholds would have increased from 2026-27, and identifies the portion attributable to the current government's freeze extension from 2028-29.

The calculator does not store your results.

Limitations of the Calculator

This tool provides an estimate of how frozen tax thresholds might affect your tax payments over time, but other factors can influence your tax bill.

For example, individuals over the state pension age may be exempt from paying NICs, and pension contributions can provide tax relief.

There are additional taxes, credits, and allowances not accounted for by this calculator.

It applies only to employees in England, Wales, and Northern Ireland. Scotland has different tax bands and thresholds.

The calculator does not apply to self-employed workers, who are taxed differently.

Assumptions on Earnings Growth

The calculator assumes your salary will increase in line with the OBR's forecasts for average weekly earnings growth each financial year. These forecasts represent the OBR's best estimates, but actual wage growth may vary.

It also assumes a consistent salary without fluctuations or job changes, which could otherwise affect earnings growth.

Assumptions on Tax Threshold Growth

The calculator uses Consumer Prices Index (CPI) inflation figures, as employed by the OBR, to estimate how tax thresholds would have risen in the absence of the freeze. Actual inflation may differ.

The personal allowance (PA) is rounded up to the nearest £10, and the basic rate limit is rounded up to the nearest £100. The additional rate threshold increases in line with the PA, which decreases by £1 for every £2 earned over £100,000.