Interest Rates Expected to Remain at 3.75%

The Bank of England is anticipated to maintain the base interest rate at 3.75%, as uncertainty continues to influence both the UK and global economies.

Analysts widely expect the benchmark rate to remain unchanged due to clear indications from the Bank that it will take time to evaluate the economic and cost-of-living impacts stemming from the ongoing conflict in the Middle East.

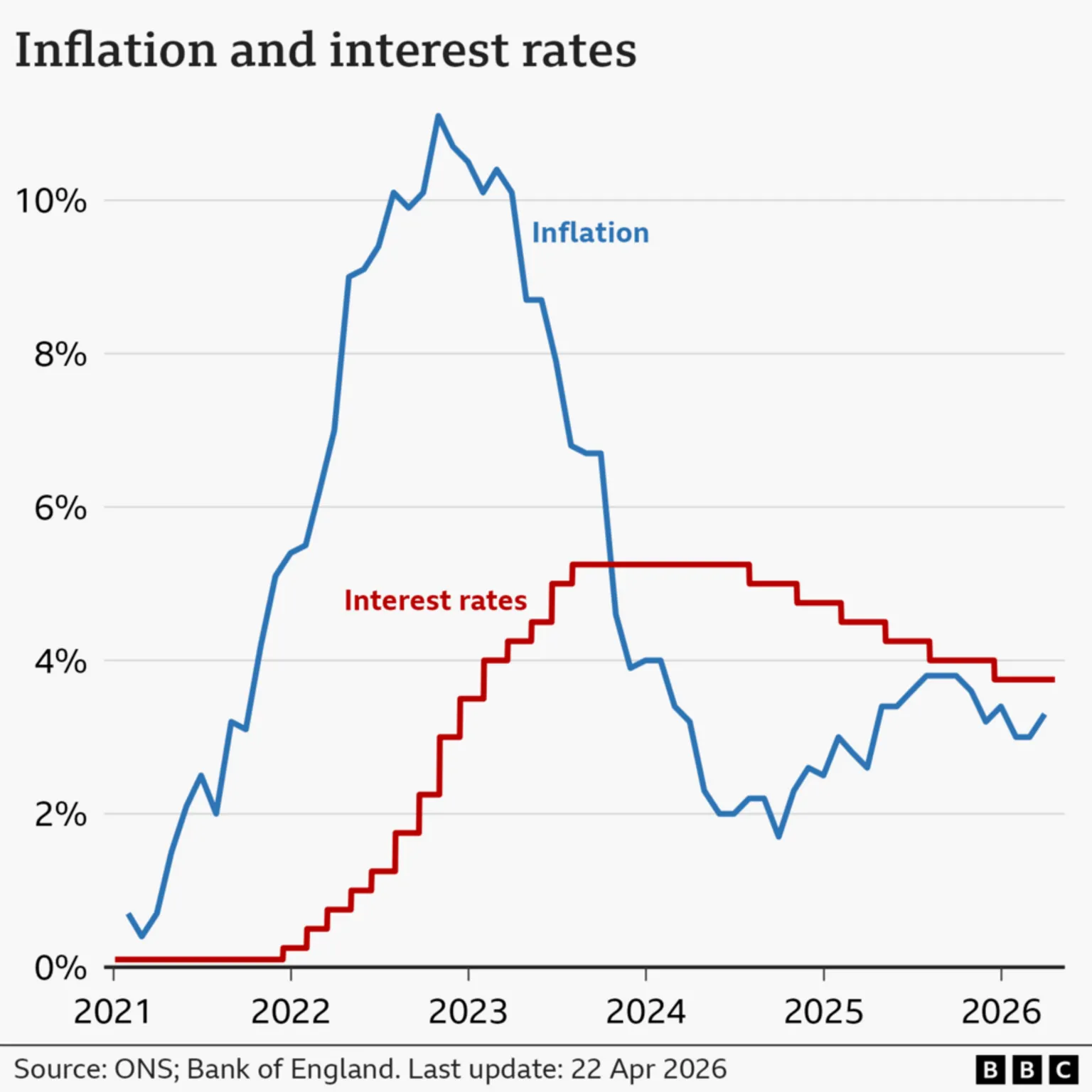

The base rate serves as the Bank's principal mechanism for controlling inflation, which measures the annual increase in prices for goods and services.

Currently, inflation stands at 3.3%, exceeding the 2% target, but the Monetary Policy Committee (MPC) is expected to adopt a cautious stance.

"The repercussions of the [Iran] conflict are still keenly felt and uncertainty about how the situation could evolve also remains high, which will be key points the Monetary Policy Committee (MPC) will have to consider,"said Sandra Horsfield, economist for wealth management group Investec.

Monetary Policy Report and Economic Forecasts

The MPC's decision will be announced at 12:00 BST, accompanied by the publication of its first comprehensive monetary policy report and economic forecasts since the US-Israeli strikes on Iran commenced in late February.

The Bank is unlikely to provide definitive guidance on the future trajectory of interest rates at this time.

Commentators note considerable uncertainty persists for the remainder of the year, with some suggesting that rate increases remain possible, while others anticipate no change.

Prior to the US-Israel attack on Iran, economists had forecasted a decline in both inflation and interest rates during the year.

Impact on Borrowers and Savers

The MPC's decision affects borrowers, savers, and the investment and hiring decisions of businesses.

The conflict in Iran has contributed to increased mortgage costs for homeowners securing new fixed-rate deals.

For borrowers, the interest rate on a fixed mortgage remains unchanged until the deal expires, typically after two or five years, at which point a new rate is selected.

At the onset of the conflict, the average rate on a two-year fixed mortgage was 4.83%, rising to a peak of 5.90%, according to financial information service Moneyfacts. It has since decreased slightly to 5.81%.

Several lenders have announced rate reductions within the past 24 hours; however, brokers caution that further fixed-rate increases in the coming weeks cannot be ruled out.

"The standard advice in uncertain economic times stands: secure a mortgage rate you think suits your circumstances or looks reasonable value for money as soon as you can, then try to switch to a cheaper deal with the lender before your mortgage is due to complete,"said Aaron Strutt, from mortgage broker Trinity Financial.

Savers are also closely monitoring the MPC meeting outcome.

Interest rates on approximately half of UK savings accounts exceed the current Bank of England benchmark rate of 3.75%, but those who have not switched providers for an extended period often receive less favorable rates, according to Moneyfacts.

If prices rise sharply, the purchasing power of savings diminishes, especially when interest earned on those savings is low.